If you’ve ever wondered what the average cost of car insurance in Texas actually is, the answer isn’t as simple as one number. Rates across the state run higher than most of the country, and if you’re in the Dallas Fort Worth area, you’re likely paying above that state average. What makes it confusing is how much those numbers can vary from one driver to the next. Two people with similar cars and similar coverage can end up with very different premiums.

This guide breaks down what drivers in Texas are paying right now, why those costs are higher here, and what factors push your individual rate up or down. Once you understand that, it becomes a lot easier to make sense of your own policy and where you might be able to adjust it.

Key Takeaways

- Texas full coverage averages around $2,190 per year — above most states, with DFW running higher than the state figure.

- Hail is the single biggest cost driver in north Texas. The DFW corridor is one of the most hail-active areas in the country.

- Age, driving record, credit score, and vehicle type all push individual rates above or below the average significantly.

- Rates for the same coverage vary considerably between carriers. Most drivers have never actually compared.

What Is the Average Car Insurance Cost in Texas?

The national average looks worse than it is because Florida, Michigan, and Louisiana drag it up. Take those out and the typical state sits meaningfully below Texas. Minimum coverage stays close to national because Texas’s 30/60/25 liability requirement isn’t that different from most states. The real gap is full coverage — that’s where weather and repair costs do their damage.

Source: Bankrate, 2024 Average Car Insurance Rates

Why Is Car Insurance So Expensive in Texas?

The short and complicated answer: Hail. That’s the answer for north Texas, and most people don’t fully grasp how much it drives their rate.

DFW sits in a corridor where large hail isn’t a freak event — it happens most years, sometimes more than once. Storm researchers have a name for it: hail alley. A single significant storm can generate thousands of comprehensive claims across the metro in an afternoon. The spring of 2023 produced billions in insured hail losses across Texas alone. Insurers price that claim volume into every comprehensive premium sold in the region. When you’re paying for comprehensive in Garland or Sachse, part of what you’re covering is the last storm. Part of it is the next one.

Everything else is secondary, but it stacks. Texas has five of the 25 most congested cities in the country. More time in traffic means more low-speed collisions, more claims, higher rates. About 20% of Texas drivers are uninsured — when they cause accidents, those costs don’t disappear. They get distributed across insured drivers through rate adjustments. Flooding hits Houston hard and DFW worse than most people expect. And repair costs on modern vehicles have climbed sharply — sensors, cameras, and proprietary parts have turned what used to be a $900 bumper repair into a $3,500 job. None of it is getting cheaper.

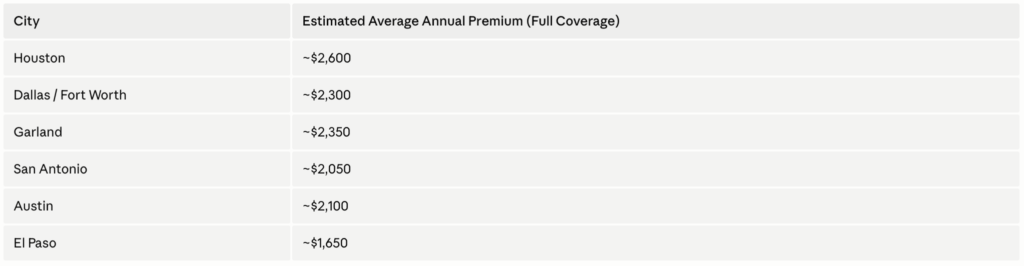

Average Car Insurance Cost by City in Texas

Where you live inside Texas moves your rate as much as living in Texas at all.

Estimates based on Bankrate and industry data, 2024. Individual rates vary.

Houston leads because Harris County has both the worst flooding exposure in the state and some of the highest claim frequency overall. El Paso sits at the bottom — drier climate, lower theft rates, and lighter traffic relative to its size.

Garland tracks just above the DFW average. Urban claim frequency plus hail corridor exposure. A driver in Garland pays more than someone in Lubbock or Midland not because of how either one drives, but because of where they live and what the claims data looks like for that geography. The insurance company isn’t making a character judgment. They’re pricing what they see.

What Affects Your Individual Car Insurance Cost in Texas?

The state averages don’t tell you much about your specific number. A few things move it dramatically.

Your driving record is the biggest lever. A clean record in Texas can put you well below the state average. One at-fault accident and you’re above it, usually by a meaningful amount, and that mark sits on your record for about three years. Two incidents over five years and you can be looking at rates close to double what a clean-record driver pays in the same zip code.

Age creates the most extreme spreads of anything on this list.

Estimates based on industry data, 2024. Clean driving record assumed.

Teen rates aren’t a punishment — they reflect consistent claim data across every carrier. It’s not about any one teenager. The drop from 19 to 25 is steep if the record stays clean. From the mid-twenties through the mid-fifties, rates flatten out and stay relatively stable.

Credit score catches people off guard. Texas allows insurers to use a credit-based insurance score as a rating factor. It’s not identical to your lending credit score but uses similar underlying data, and it can swing a premium in either direction. For drivers with poor credit, it can add more to the annual rate than a moving violation would. Most people don’t know that.

Vehicle type matters less because of the car’s sticker price and more because of repair costs. A newer truck with embedded sensors and driver assistance technology can cost $4,000–5,000 to repair after a parking lot collision. Same-price vehicles carry different premiums because the parts and labor costs behind them are different.

How to Lower Your Car Insurance Cost in Texas

The move that produces the most consistent results — and the one most people skip entirely — is actually comparing rates across carriers. Not checking one company’s website. Not calling a captive agent who can only quote their own products. Pulling quotes from multiple insurers for identical coverage and seeing what comes back.

The spread between carriers for the same driver and same coverage in Texas can run $300–600 a year. Drivers who’ve been with the same company for several years often have no idea what the current market looks like for their profile. Nobody at the carrier is going to bring that up. An independent agency runs the comparison across multiple carriers at once — that’s the practical difference between going direct and not.

After that:

Bundling auto with homeowners or renters under the same carrier almost always produces a discount. It’s one of the more consistent savings available, worth asking about even mid-policy.

Raising the deductible lowers the premium. The limit is practical — whatever the deductible is set at has to be a number you could actually cover if something happened this week. Choosing $2,000 to save $15 a month doesn’t work if $2,000 isn’t accessible.

Ask about discounts specifically. Good driver, defensive driving course, low annual mileage, autopay, paid-in-full. The defensive driving course takes a few hours online and the discount applies immediately on most policies. Not all discounts get applied automatically. Some require a prompt.

For older paid-off vehicles, run the collision math. If the car is worth $5,000 and the deductible is $1,000, max payout on a total loss is $4,000. If collision coverage costs $700 a year, you’d need a claim roughly every six years to break even — not counting what filing does to your rate. At some point on an older vehicle, carrying that risk yourself is the smarter financial call.

Frequently Asked Questions

1. Is car insurance required in Texas?

Yes — 30/60/25 minimum liability. That’s $30,000 per injured person, $60,000 per accident, and $25,000 in property damage. Driving without it means fines starting at $175, possible license suspension, and impoundment. And if you cause an accident without coverage, every dollar of damage is yours personally.

2. Why is Texas car insurance so expensive?

Hail is the lead factor for anyone in north Texas. DFW sits in one of the highest hail-frequency corridors in the country and carriers price that into every comprehensive premium sold here. Stack on heavy urban traffic, flooding, a 20% uninsured driver rate, and repair costs that have roughly doubled on modern vehicles — it adds up fast.

3. Does Texas have no-fault insurance?

No. At-fault state. Whoever caused the accident is financially responsible for the damages. The injured party can file against the at-fault driver’s liability, use their own policy, or take it to court.

4. What’s the cheapest way to get car insurance in Texas?

Minimum liability gets the premium as low as it goes. But minimum coverage runs out quickly in a serious accident and you’re on the hook for everything above it. The more useful question is how to get solid coverage for less money — and the answer is comparing across carriers, which consistently produces bigger savings than any other move.

5. Will my rate go down as I get older?

Through your mid-thirties, yes. The jump between teen rates and mid-twenties rates is dramatic — often 40–50% or more with a clean record. From about 30 to 55, rates flatten out. They tick back up slightly after 65 as claim frequency rises again. The driving record matters more over time than the birthday.

If you’re in Garland, Sachse, or anywhere in the DFW area and want to see what the current market actually looks like for your coverage, reach out to Bickerstaff Insurance. We’re independent, we work with more than 15 carriers, and we’ll run the comparison. Get a quote here.